Posted on April 10, 2024 by Bessie Daschbach

On March 6, 2024, the U.S. Securities and Exchange Commission (SEC) issued its long-awaited climate disclosure rule. The rule, formally titled, “The Enhancement and Standardization of Climate-Related Disclosures for Investors,” came nearly two years after the SEC’s initial proposal and after some 24,000 public comments in response to that proposal.

In line with the initial proposal, the final rule requires companies to make disclosures as to (1) climate-related financial risks, (2) climate-related transition plans, and (3) greenhouse gas emissions. But, the final rule also deviates from the initial proposal in significant ways. Foremost among those is the rule’s exclusion of any requirement to disclose Scope 3 emissions. Also in contrast to the initial proposal, the final rule requires disclosure of Scope 1 and 2 emissions only in the event they are found to be material and exempts smaller publicly-traded companies from the obligation to report emissions at all. Also of note, the rule eliminated a provision in the proposal requiring companies to disclose board member expertise around climate concerns.

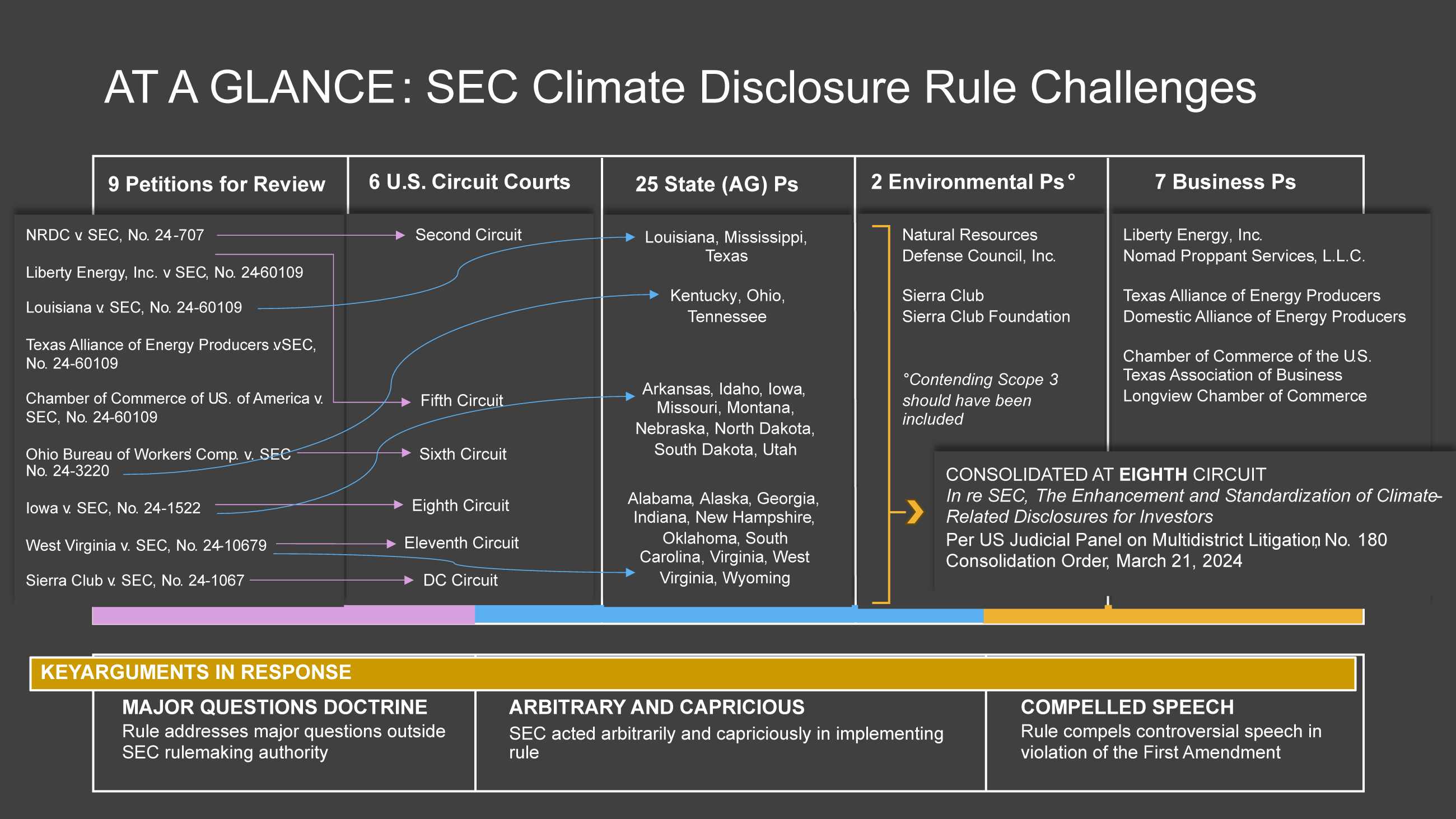

The final rule has been described as scaled-back and even diluted in comparison to the initial proposal. But, the contours of the rule in contrast to the proposal is only part of the story unfolding. A slew of legal challenges to the rule have been asserted and are taking center stage. Fairly immediately, nine petitions for review were filed in six different U.S. Circuit Courts. Of those nine petitions, seven seek to strike the rule as overreaching, while two filed by the Natural Resources Defense Council, Inc. and the Sierra Club/Sierra Club Foundation contend Scope 3 should have been included. Petitioners opposing the rule wholesale include Republican attorneys general from 25 states together with private business interests—both individual business interests and a handful of business alliances. Key arguments asserted in response to the rule include those based on the major questions doctrine—that is, that the rule addresses major questions around climate and emissions outside the ambit of the SEC’s rulemaking authority—as well as contentions that the rule compels controversial speech in violation of the First Amendment and that the SEC acted arbitrarily and capriciously in implementing the rule.

The nine petitions proceeded independently for only a short time. On March 21, 2024, by order of the U.S. Judicial Panel on Multidistrict Litigation (and following random selection), the nine petitions for review were consolidated in the U.S. Court of Appeal for the Eighth Circuit. All eyes are now on that case and how the court will take up the arguments made in response to the rule. Meanwhile, on April 4, in a somewhat unexpected turn, the SEC announced it would suspend implementation of the rule pending disposition by the Eighth Circuit.

As summarized by the Judicial Panel on Multidistrict Litigation’s own website, the purpose of centralizing cases is to “avoid duplication of discovery, to prevent inconsistent pretrial rulings, and to conserve the resources of the parties, their counsel and the judiciary.” Notably, “[t]ransferred actions not terminated in the transferee district are remanded to their originating transferor districts by the Panel at or before the conclusion of centralized pretrial proceedings.” Given that, tracking the original nine petitions for review could still be of some consequence. But, with so many of them and the nuances among them, that is no small task. Check out this visual reference for a head start:

In addition to the consolidated petitions now pending at the Eighth Circuit, note that Liberty Energy, Inc. and Nomad Proppant Services, L.L.C. have since filed a second challenge to the rule—again in the U.S. Fifth Circuit, specifically the U.S. District Court for the Northen District of Dallas. The stated aim in doing so is solely to protect the parties’ claims in the event it is determined the Texas district court has jurisdiction over some or all of the challenges to the rule.

That backstop aside, stay tuned for more on how the case develops in the Eighth Circuit or, more to the point, how the SEC’s final rule fares.